FinTech, MedTech, EduTech and FashTech are current buzzwords and just a few examples of the current hype to merge a specific industry with the word technology. FinTech represents the combination of the words Financial (Industry) and Technology, MedTech stands for the combination of the words Medical and Technology, EduTech stands for the combination of the words Education and Technology, and FashTech stands for the combination of the words Fashion and Technology. Where does this urge to merge these terms come from?

‘X’-Tech

As previously mentioned, “FinTech”, “MedTech”, “EduTech” and “FashTech” are only four examples of industry names which are aggregated with the word technology. Other possible candidates are: “OilTech”, “AirTech” or “CanTech”. However, what do these abbreviations mean? The answer to this question is not straightforward, multiple opinions and definitions exist. In general, three different viewpoints about the meaning behind these abbreviations exist. In the remainder of this article, the financial industry is used as example but the same three viewpoints can be recognized for the medical, educational, and fashion industry.

From the first viewpoint FinTech is defined as “innovation in financial services.” The term technology is not included in this definition and is seen as an implicit driver for the mentioned innovation. The second viewpoint does not explicitly focus on innovation but highlights the use of technology. This viewpoint considers FinTech as “an organization that uses software to provide financial services.” The last viewpoint is very similar to the second viewpoint but attempts to provide a more detailed definition of FinTech, an example of a definition from this point of view is (FundThrough 2015): “FinTech is technology that serves the clients offinancial institutions, covering not only the back and middle offices, but also the front office that has been human-driven for so long.”

When the definitions of the three viewpoints are being compared, then software / technology emerges as keyword twice and innovation once. How are the terms technology (software) and innovation related to each other? New technology (software) is considered as one of the six possible innovation types. The other five innovation types are: 1) a new service concept, 2) a new kind of customer interaction, 3) a new business partner, 4) a new business model, and 5) a process, organization or culture change (Den Hertog, 2010). Each of the previous six innovation types can lead to improved financial services. However, currently the industry is especially focused on one of the six innovation types namely technology.

Altogether, FinTech can be defined as innovation which is made possible by information technology to improve current existing services or to provide new services. However, is the innovation of services by means of information technology new? Maybe, somewhere back in 1960s. So, why does ‘X’-Tech (where the X can be replaced by any industry) receives this much attention? More important, is this attention rightfully deserved for a phenomenon as old as the 1960s.

Traditional organizations and ‘X’-Tech

On July 28 of this year, Bloomberg published a news item and associated article about Goldman Sachs. The header of the article stated (Brooker, 2015): “Goldman in Ventureland: The inside story of how—and why—Goldman Sachs became a tech-investing powerhouse.” As the title of the article already indicates, it discusses why Goldman Sachs has heavily invested in technology companies.

Firstly, some numbers will be provided about the investments Goldman Sachs has conducted during the past seven years. Goldman Sachs has participated in 132 technology-oriented fundraising rounds since 2009. During the past 2,5 years, 77 investment deals are made of which 33 investment deals have taken place in the past year and 22 investment deals within the first half of this year (Brooker, 2015). So, these numbers indicate an increase in investments. Examples of organizations in which Goldman Sachs invested are: Uber, Pinterest and Dropbox. The first reason for these investments, and from the point of view of a bank also the most obvious reason, is: the economic return on investment. The article also describes a second, and perhaps a more important, reason why Goldman Sachs made these investments: the organization mainly wants to learn!

The fact that Goldman Sachs acknowledges that they need to keep track of the latest technology corresponds to the results of the annual survey of Fortune, used for determining the Fortune 500. In this survey, organizations are asked what they conceive as the greatest challenge for the coming years. The number one answer was: the rapidly changing technology and associated threats and opportunities. The second answer was: cybersecurity (also an answer related to technology). So to keep up with the technological changes, Goldman Sachs invests in technology companies. Not just for the return on investment but to learn how these organizations apply technology. The ultimate goal of these current investments for Goldman Sachs is to apply the technology herself and become better in this type of innovations. In order to optimize this learning process, Goldman Sachs is transforming both on an organizational and a cultural level.

This organizational transformation has led to an important fact: the largest division of Goldman Sachs at this moment is the technology division. This division comprises almost 33% (more than 9000 employees) of the total workforce. As a result, the bank currently employs more technical(-oriented) staff than bankers and traders (Brooker, 2015). Summarized, it can be concluded that one of the largest investment banks of the world, Goldman Sachs, conducts the purest form of FinTech herself.

If one of the largest investment banks is one of the biggest players in FinTech, then it can be stated that FinTech is absolutely nothing new. This statement would be correct if the story of Goldman Sachs was true for the entire financial sector. However, this is not the case. The story of Goldman Sachs is one of the few stories from the ‘traditional’ financial world. This is also one of the reasons why FinTech receives so much attention. Currently, not the ‘traditional’ cumbersome financial organizations innovate based on technology but especially the small startups are the ones that lead the innovation.

However, we should not speak too negatively about the existing banks and financial service providers. Like Chris Skinner expressed well in his article: “does anyone really think banks aren’t aware of fintech.” Of course banks are not ‘completely stupid’, they also see the world change. However, many organizations experience difficulties with keeping up to date with the latest technology and its associated opportunities and threats.

Why do startups seem to function better in the current FinTech environment than the traditional organizations? An unambiguous answer to this question does not (yet) exist. However, scientists and the industry agree on one point: a lot of variables may play a role in answering this question. The remainder of this article examines one variable: the composition of knowledge which a person, team, and/or organization possesses.

The ‘X’-Tech Superman

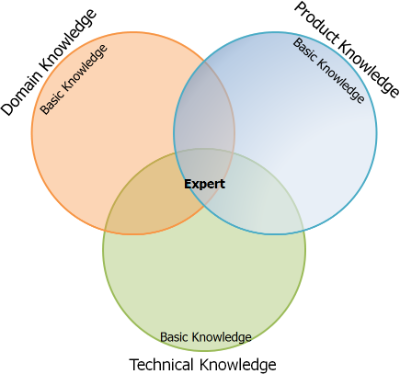

At a high level, three types of knowledge can be distinguished: product knowledge (subject-matter expertise), domain knowledge, and technical knowledge (see Figure 1).

Product knowledge corresponds to knowledge about a specific product or service in a specific industry for example: investments, personal finance or banking infrastructures in the financial industry. Domain knowledge corresponds to knowledge about a specific domain or knowledge about specific methods and techniques of a specific domain. For example knowledge about the domain Business Process Management (BPM) and/or the method Six Sigma. Technical knowledge corresponds to knowledge about the use and application of information technology (hardware and software).

In the ideal situation, one person would be an expert with regard to one or more products, domains and/or technologies. These persons are also referred to as ‘X’-tech supermen or superwomen. Taking FinTech into account, what are the characteristics of a ‘Fin’-Tech superman at this moment? Firstly, the ‘Fin’-Tech superman possesses broad and profound product knowledge about the financial sector and the underlying products and services like investments, personal finances, etc. Moreover, the ‘Fin’-Tech superman possesses thorough domain knowledge about Business Process Management, Business Rules Management, lean six sigma, machine learning, predictive analytics, cognitive techniques and preferably a dozen additional domains, techniques and/or methods. Furthermore, the ‘Fin’-Tech superman assembles its own in-memory servers. He installs and configures Spark, Hadoop, MongoDB, Mesos, Pentaho, OpenDaylight and OpenDataplane entirely by himself. Additionally, it would be very helpful if the ‘Fin’-Tech superman has 40 years of experience. Two words that summarize the above described profile are: dream on!

Despite the fact that we do not live in a dream world and no ‘X’-Tech supermen exist, there are people who partly comply with an X-tech profile. This profile implies that a person has very solid product knowledge (subject-matter expertise) and very sound technical knowledge. In other words, these persons know enough about technology to conduct a thorough conversation with the ICT staff (programmers, engineers) and on the other hand they also have sufficient subject-matter expertise about the business in which they operate. Several venture capitalists and angel investors impose the condition, before they invest, that at least one of the founders fits this latter described profile or in some cases that at least the founders together can cover the profile.

Fred Wilson, a venture capitalist, describes in his article “the new tech CEO archetype” that: the combination of product knowledge and technical knowledge is the new profile for a CEO of a ‘technical-oriented’ organization. He provides the following examples of CEOs: Marissa Mayer (Yahoo), Satya Nadella (Microsoft), and Sundar Pichai (Google). With regard to Goldman Sachs, Martin Chavez is the current CIO and acts as a bridge between the Tech-Scene and the bank. Chaves has founded and sold his own Silicon Valley startup and receives the respect of the Tech-Scene and speaks their language (Brooker, 2015).

FinTech, MedTech, EduTech, FashTech are buzzwords but innovation by means of technology will persist and will (at an accelerated pace) continue. Not only startups will innovate but also the ‘traditional’ companies are forced to innovate. This means that is becomes more and more important to form teams which possess product, domain, and technical knowledge to be able to keep up with the velocity of innovation. In general, this will be easier for startups than for ‘traditional’ companies.

Co-Author: Eline de Haan

References

Brooker, K. (2015). Goldman in Ventureland: The inside story of how – and why – Goldman Sachs became a tech-investing powerhouse. Retrieved 30-07-2015, 2015

Den Hertog, P. (2010). Managing service innovation: firm-level dynamic capabilities and policy options. http://dare.uva.nl/document/184618.

Skinner, C. (2015). Does anyone really think banks aren’t aware of the Fintech challenge? Retrieved 2015-08-12, 2015

Wilson, F. (2015). The New Tech CEO Archetype. Retrieved 2015-08-06, 2015